Similar to revenue recognition, there are many intricacies surrounding expense recognition. Generally, companies recognize expenses by the accounting period in which it consumes the expenditure. One principle or concept that is associated with expense recognition is matching costs businesses incur with revenue they recognize, as long as the revenues and expenses relate to the same transaction. A common example of when this concept is used is when companies buy and sell inventory, and have to calculate the cost of their goods sold. In many instances, companies buy inventory in cash but are unable to sell it completely in the same period: companies purchase inventory in one period to be sold either in the same period or a different period, and carry unsold inventory throughout different accounting periods.

This article explains the four different inventory costing methods: specific identification, first in first out (FIFO), weighted average cost, and last in first out (LIFO). Companies should always try to use the inventory costing method, which best matches the physical flow of their inventory; however, there are situations where the different methods could be beneficial when it comes time to pay their income taxes.

Specific Identification Method

The specific identification method recognizes inventory based on the movement of specific items. Companies that use this method are often able to track and retrieve each item of inventory easily, as well as be able to record the cost of each item. This method is popular among companies with large, unique, or costly items in their inventory. An example of a company that uses this method would be an exotic car or plane manufacturing firm that builds a very limited number of expensive products (think of Pagani and Boeing as examples).

FIFO: First In, First Out

As the name of this method implies, if a company uses FIFO, the inventory that is either manufactured or purchased first is sold, used, or disposed of first, and the inventory is sold in the order it is purchased. FIFO is allowed under both IFRS and GAAP accounting standards, and can offer tax benefits depending on the outlook of the current economy.

If the economy is going through a phase of inflation, then reporting under FIFO will overstate their earnings. This is true because when they purchased their inventory, they received it at a price much lower than they could replace it for in the present, and because of inflation the price at which they sell their goods will also be increasing. Under FIFO, they will have to pay more income taxes during a time of strong inflation.

LIFO: Last In, First Out

LIFO is the complete opposite of FIFO: the last item purchased is the first item sold. This is usually the opposite of the physical flow of inventory, but there are some exceptions. This method is permitted under US GAAP, but is not permitted under IFRS.

In an inflationary environment, LIFO earnings will be lower than FIFO earnings, which translates to less income taxes paid. In a time of high inflation, the price paid to acquire goods will be closer to the price sold, which equates to a higher cost of goods sold, lower gross income, and lower net income.

LIFO Liquidation

The main benefit of the LIFO valuation method is that it accurately matches prices paid for inventory with current revenue. This ultimately lowers the company’s tax burden because of a higher COGS compared to the other methods which decreases earnings before tax. However, in some instances, a company is forced to use older and older inventory because current sales outpace the purchase of new inventory. When this occurs, companies will end up having a higher tax liability because of a decrease of COGS and an increase in their gross and net income, which is the opposite effect of what the company was trying to accomplish in the first place.

Average Cost

The average cost method of valuing inventory is the most simple. The average cost of a unit is determined by dividing the total cost of goods available for sale by the total quantity available for sale. This method is allowed under both US GAAP and IFRS.

Example:

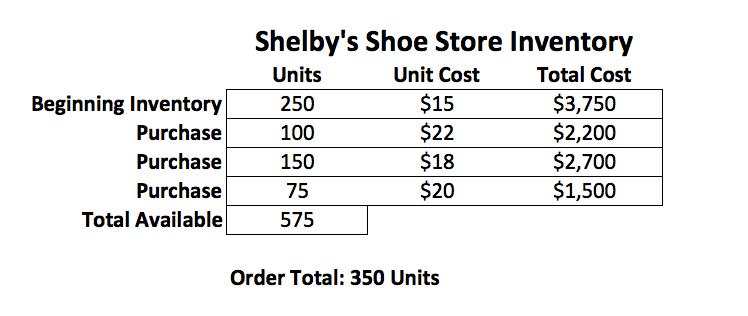

Shelby’s Shoe Store is a supplier of shoes to retail stores. They purchase bulk orders directly from the manufacturer, and then sell them at a premium to small sports and apparel retailers. Below are the inventory related transactions that have occurred in the last year. Shelby’s just received an order for 350 units. Cost of goods sold and the value of the ending inventory after the transaction occurs is calculated below.

FIFO: 250 units at $15, and 100 units at $22, will be sold.

COGS: (250 x 15) +(100 x 22) = $5,950

Ending Inventory: (150 x 18) + (75 x 20) = $4,200

LIFO: 75 units at $20, 150 units at $18, 100 units at $22, 25 units at $15, will be sold.

COGS: (75 x 20) + (150 x 18) + (100 x 22) + (25 x 15) = $6,775

Ending Inventory: 225 x 15 = $3,375

Average Cost: Find the weighted average cost of one unit:

(250 x 15) + (100 x 22) + (150 x 18) + (75 x 20) = $10,150/575 = $17.65

COGS: 350 x 17.65 = $6,178.26

Ending Inventory: 225 x 17.65 = $3,971.25

As you can see by the calculations, different inventory valuation methods equate to different COGS and ending inventory amounts.

Summary

When deciding on an inventory valuation method, companies need to be aware of everything this decision could affect, such as COGS, which ends up affecting gross income, and the amount a company ends up paying in income taxes. Companies also need to look at the amount of inflation occurring in the economy before choosing a valuation method. Questions? Leave a comment.

Pingback: Exploring the Differences Between IFRS and GAAP -

Pingback: The Rise of Dropshipping: A Game-Changer in E-Commerce -

Pingback: When You Should Lease Storage Solutions for Your Business - The Daily CPA