When determining how much life insurance you need, consider what life stage you are currently in as well as your circumstances. Your marital status, number of dependents, financial obligations, and intentions to pass on your property can impact your insurance needs. It also depends on what you are using life insurance for.

Income Replacement

Many times, life insurance is used as an income replacement if the income generating family member should pass away. When determining the amount needed for income replacement, a few things should be considered:

Do you want the life insurance proceeds to be income for a set number of years, or do you want it to be enough to fund a lifetime of income?

- There are a few ways to calculate this – the first method, the income rule, multiplies your gross annual salary by a factor of five or ten. A factor of five assumes the beneficiary will draw both principal and interest from the insurance proceeds. A factor of ten may allow your beneficiaries to draw on interest only.

- For a more specific calculation, determine what pieces of your income will be needed if you pass away. Income to replenish emergency funds, to pay off a mortgage, for college funding, car payments, general living expenses, etc. This way, you can back into an appropriate number of what you believe would need to be replaced. Remember to take into account inflation (if there is no growth in the policy itself) and the changes in your family’s spending needs as time goes on.

Special Funding Needs

Determine what length of time your special funding need exists:

- For example, if you decide you need a life insurance policy to cover your mortgage debt obligation, that value is only decreasing. This could be split up with laddered term policies to keep the costs down and death benefit in correlation with the mortgage.

- If the special funding need is college tuition for children, for example, this value is only increasing. This might be best with a type of permanent policy that offers growth from within the policy, such as a Universal Life policy. If you have time to let a policy take its course, it can keep up with increases in spending quite well.

Life Insurance Premiums

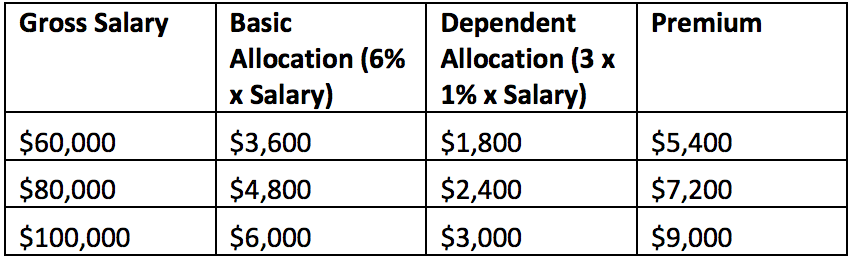

What about using the premium to determine the life insurance amount? You could relate your current income to an affordable life insurance premium. A rule of thumb is 6 percent of your salary plus an additional 1 percent of your salary for each dependent. For example, assume Mr. Doe has a non-working spouse and two children (i.e., three dependents). The insurance premium allocations would be as follows:

Conclusion

The advantage of using these rules to determine your life insurance needs is the simplicity. They help you find a rough starting point. The drawback, however, is that these rules fail to consider the specific needs and circumstances of each individual. There is no consideration given for the ages of your dependents or whether your family has more than one income. They also don’t address liquidity needs for estate planning or the existence of special needs children.

The worst mistake you can make with life insurance is failing to recognize the financial impact of your death. If you were to suddenly pass away, the last thing you would want to do is leave your family in a difficult financial situation. Unfortunately, most people are underinsured, and many who are insured fail to review their existing policies, which can result in insufficient levels of insurance.

Your financial professional can provide you with a more concrete projection of your life insurance needs. For more on the types of life insurance and how they are best used, see my next post in the Life Insurance series coming soon!

Kelsey Dolfi, CPA. RiverStone Private Wealth Advisors, 7 Livingston St. Rhinebeck, NY 12572. 845- 516-4440. kdolfi@riverstonepwa.com Securities offered through Commonwealth Financial Network, Member FINRA/SIPC.

When determining how much life insurance you need, consider what life stage you are currently in as well as your circumstances. Your marital status, number of dependents, financial obligations, and intentions to pass on your property can impact your insurance needs. It also depends on what you are using life insurance for.

Income Replacement

Many times, life insurance is used as an income replacement if the income generating family member should pass away. When determining the amount needed for income replacement, a few things should be considered:

Special Funding Needs

Life Insurance Premiums

What about using the premium to determine the life insurance amount? You could relate your current income to an affordable life insurance premium. A rule of thumb is 6 percent of your salary plus an additional 1 percent of your salary for each dependent. For example, assume Mr. Doe has a non-working spouse and two children (i.e., three dependents). The insurance premium allocations would be as follows:

Conclusion

The advantage of using these rules to determine your life insurance needs is the simplicity. They help you find a rough starting point. The drawback, however, is that these rules fail to consider the specific needs and circumstances of each individual. There is no consideration given for the ages of your dependents or whether your family has more than one income. They also don’t address liquidity needs for estate planning or the existence of special needs children.

The worst mistake you can make with life insurance is failing to recognize the financial impact of your death. If you were to suddenly pass away, the last thing you would want to do is leave your family in a difficult financial situation. Unfortunately, most people are underinsured, and many who are insured fail to review their existing policies, which can result in insufficient levels of insurance.

Your financial professional can provide you with a more concrete projection of your life insurance needs. For more on the types of life insurance and how they are best used, see my next post in the Life Insurance series coming soon!

Kelsey Dolfi, CPA. RiverStone Private Wealth Advisors, 7 Livingston St. Rhinebeck, NY 12572. 845- 516-4440. kdolfi@riverstonepwa.com Securities offered through Commonwealth Financial Network, Member FINRA/SIPC.

Share this:

Like this: